5 steps for buying a home in the next 5 years

Buying a home is one of the biggest and most important investments you’ll make in your life (did someone say adulting?). It’s still the single largest source of savings for Canadian households, since every payment you make builds equity.

If buying a home is in your 5 year plan, there’s some key steps you should take to make sure you reach your goal and get those dream digs.

Know your current credit score and improve it

You might not realise how much your credit score matters when buying a home. Ultimately, having a high credit score could mean you qualify for a higher mortgage. A good rule of thumb: if your credit score is between 620 to 680 you’ll qualify for a good mortgage product - BUT if it’s 680 and above you’ll qualify for a significantly better mortgage. So, get your credit score looking good before you apply for a mortgage.

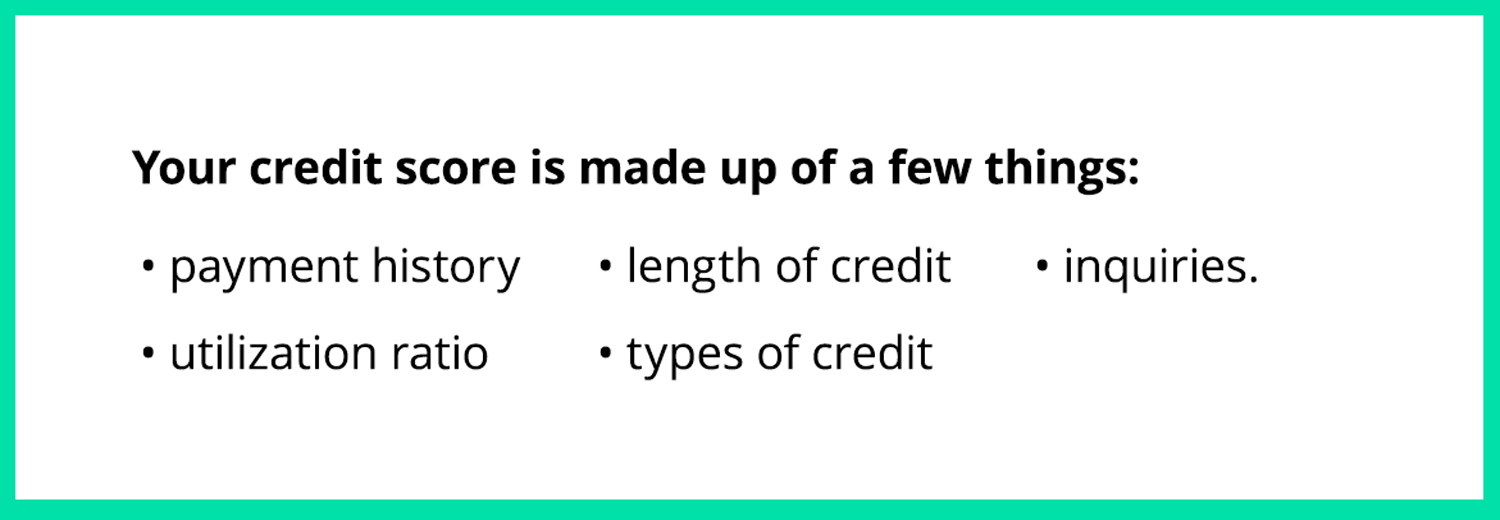

If your score is below 680, good news: you can improve it. If it’s low strictly because of debt utilization ratio, it could improve in as little as 30 days if you pay down your credit card balance so it’s below 70% of the maximum limit. Paying down your debt mid-month instead of waiting until the end of the month will also help increase your score faster. If your score is low because of your payment history, it should gradually improve over about 12-18 months with on-time payments.

Unlike the mortgage rule changes that have come into effect over the past year, having a strong credit score is in your control. So, if you’re planning on owning a home, it’s a great place to start.

Figure out what you can afford

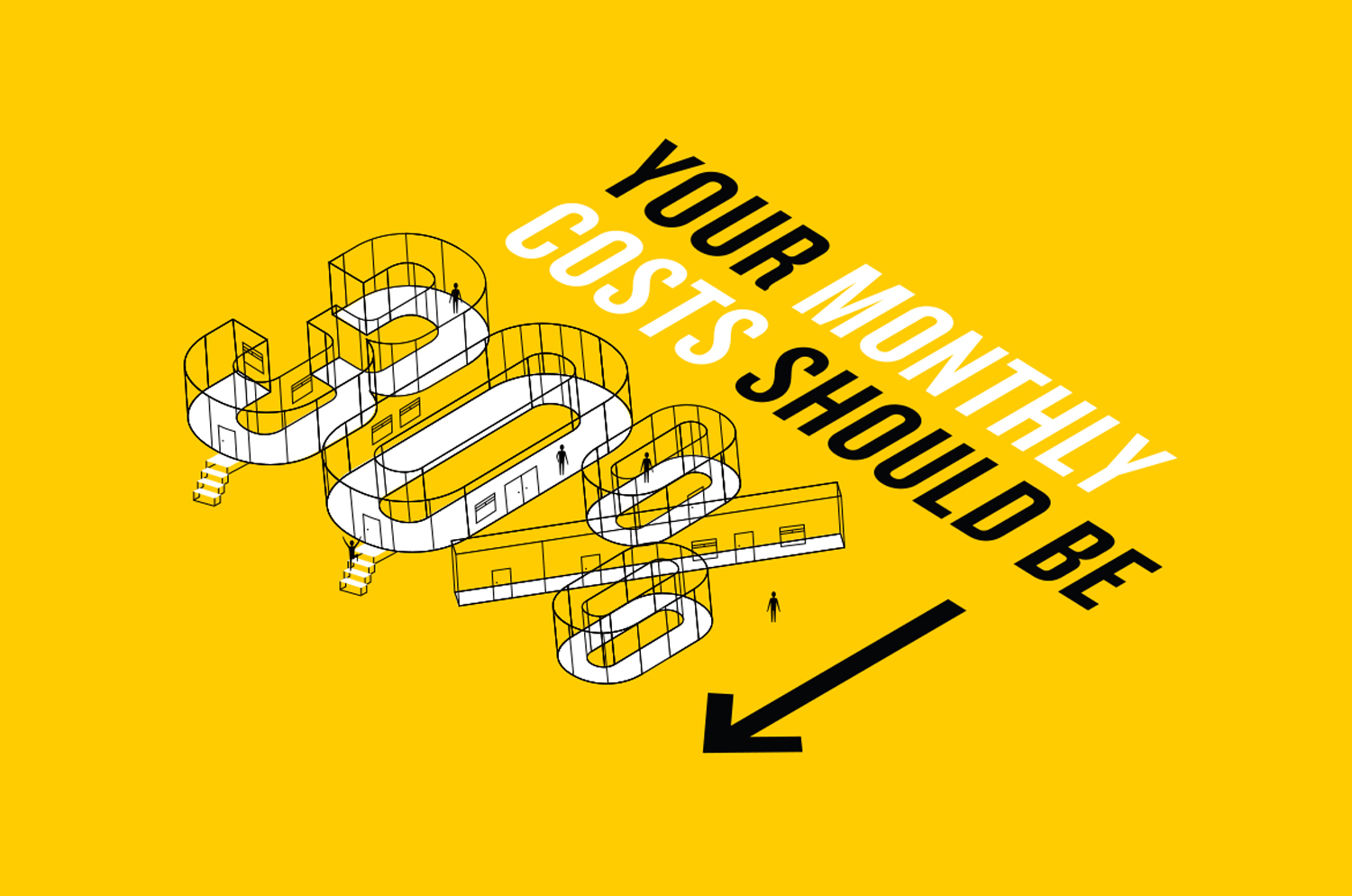

There’s a lot of economists out there that say your monthly housing costs should not exceed 30% of your gross monthly income. That should take into account all your housing costs, not just your mortgage payments. So take into account your property taxes, utilities, and insurance on top of your principal and interest payments when you’re doing the calculation.

Lenders use a similar equation to determine how much you qualify for. They want to know how much of your income will be used to pay down your current debt.The two ratios used are Gross Debt Servicing (GDS) and Total Debt Servicing (TDS). Typically they want your GDS to stay under around 32%. GDS is the percentage of your gross income that’s required to cover housing costs. These costs include: mortgage payment, property tax payment, heating expenses, and strata fees.

Basically, a low credit score could knock off 4% of qualifying room for a mortgage. Based on the median total income of Canadian families, listed as $79,000 (from Statistics Canada 2014), that could be a difference of about $27,000 on your mortgage.

Don’t forget to consider other debts you have. These will matter when your lender determines your mortgage amount. For example, a $400 monthly car debt means $100,000 less in your mortgage qualification. Or a $100 monthly credit card payment, could amount to $25,000 less in a mortgage loan, based on today’s rates. In some cases it’s better to pay down your debt than put that money towards a bigger down payment.

If you do have debt, make sure you pay off your highest interest debt (like credit cards) first.

Save for a down payment and closing costs

A great way to make sure you’re in a mortgage situation you can afford, is by putting down a decent down payment. Your down payment must be at least 5% if your purchase price is under $500,000, but if you’re able to put down more this could make homeownership more affordable. An added benefit: If you’re able to put down 20% you won’t have to pay for mortgage insurance.

An option for your down payment is the use of RRSPs. If you’re using RRSPs for your down payment you’re able to withdraw up to $25,000 to be used toward your down payment. Another option recently introduced in BC is the homebuyer's loan program, a provincially backed loan program that will match the amount that first-time buyers have saved for a down payment — up to $37,500, or five per cent of the home’s purchase price.

There are also several closing costs associated with buying a home that you’ll want to be prepared for. These include property transfer tax (which you could be fully or partially exempt from as a first time home buyer), GST, Insurance, Legal fees, and Property appraisal. These costs are different for every province, so do your research early so you can start saving.

Have other savings in place

Mortgage lenders will want to see you’re not living paycheque to paycheque, so make sure you have some kind of savings in place. This could be in the form of a TFSA (tax free savings account), which is a great option because you won’t have to pay any tax when you withdraw the money. If you’re on a tight budget, the best way to save is to set up an automatic withdrawal plan and a set monthly amount. That way you won’t be tempted to allocate the amount to something else, come pay day.

Make sure to also consider other goals you have in your life. Do you want to retire? Do you want to take a trip every year? Make sure you not only have an emergency savings fund, but are also saving for your other financial goals.

Get preapproved for a mortgage

A mortgage pre-approval is when your lender reviews your basic financial information (credit score, income, etc.) and determines the maximum mortgage amount they’re able to give you. You should consider getting pre-approved before you start looking for a home, because it’ll give you insight into what you can afford and will start the application process so you’re prepared when you find your dream home.

Building wealth through homeownership is one of the smartest investments you can make. If owning a home is one of your goals, it’s important to plan ahead.