New Year's Money Remedy #3: Get your utilization ratio in check

In our first blog post in the New Year’s Money Resolutions series we talked all about facing your holiday credit card debt head on (and what to do about it). Check it out here for a refresher.

If you’re like a lot of Canadians and you blew the budget over the holidays, let’s talk about that credit card that’s maxed to the limit....

Maxing out your your credit card has a negative impact on your credit score. And we’re not just talking about the 46% of Canadians who carry a monthly credit card balance. That includes you punctual peeps who pay it off every month. Your debt “utilization ratio” (aka your level of indebtedness, or how much of your total available credit you’re using) makes up approximately 30% of your overall credit score. Say what? ...We know what you’re thinking, Why didn’t anyone tell you this!?!

Well, now that the bad news is out of the way, here’s the good news: Fixing your utilization ratio is one of the fastest ways to fix your credit score if it’s not so hot, or even just needs a little improving. You just need to start practicing good utilization ratio habits and your score could improve in as little as 30-60 days.

It’s actually pretty simple:

For example, if your credit card limit is $1,000 and your balance is $1,000, your utilization ratio is 100 per cent — and this not good in the eyes of the credit bureau. Credit bureaus base credit scores on behaviour with credit. If you're constantly maxing out your credit cards, it could imply that you're not far away from defaulting on your minimum payments. It looks like your income is stretched.

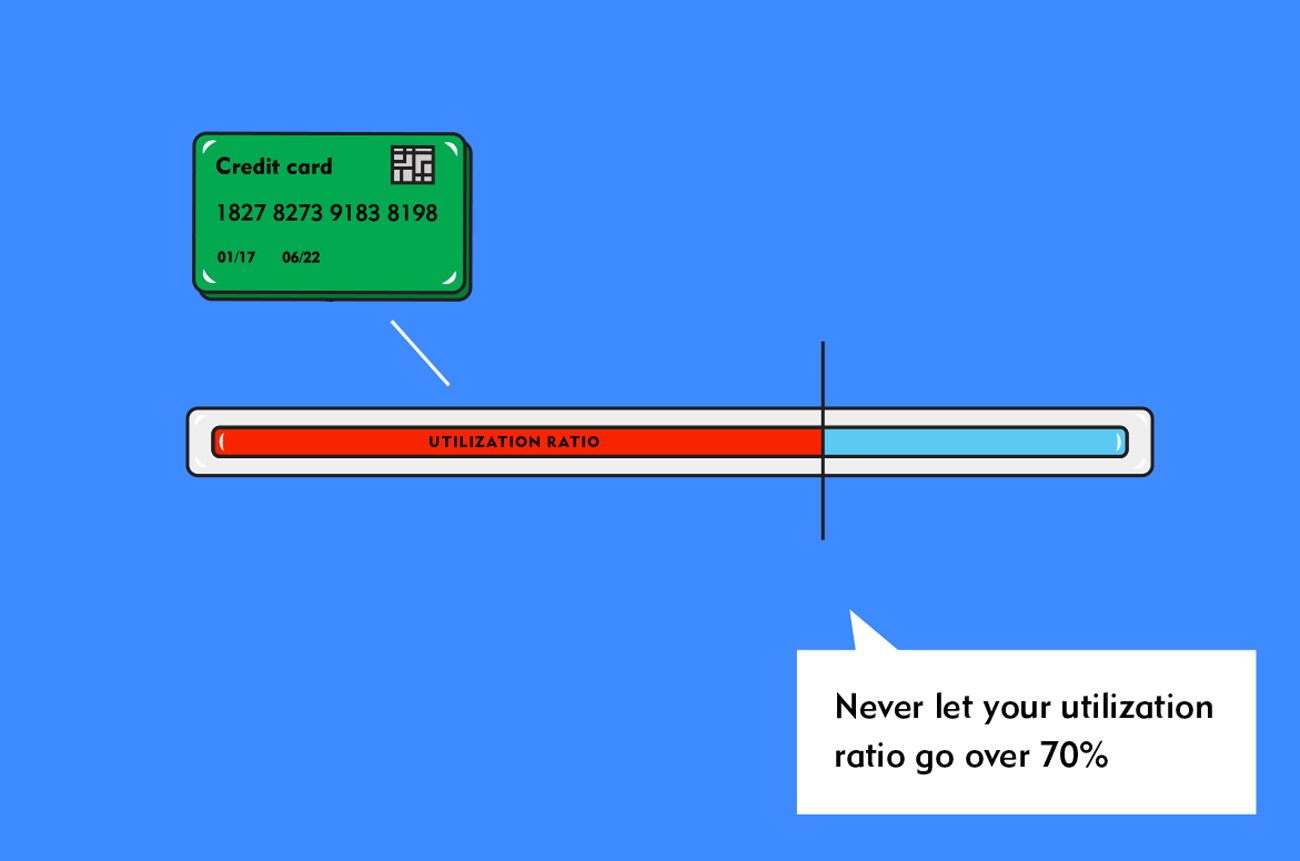

If you’re great at paying your credit card off every month…

you still don’t want to max out your limit. Say you pay it off at the end of every month, but your credit card company reports your balance to Equifax (the largest credit bureau in Canada) two days before you pay the balance off in full. When your score is calculated, it’ll show that you maxed out your card. So, never let your utilization ratio go over 70%.

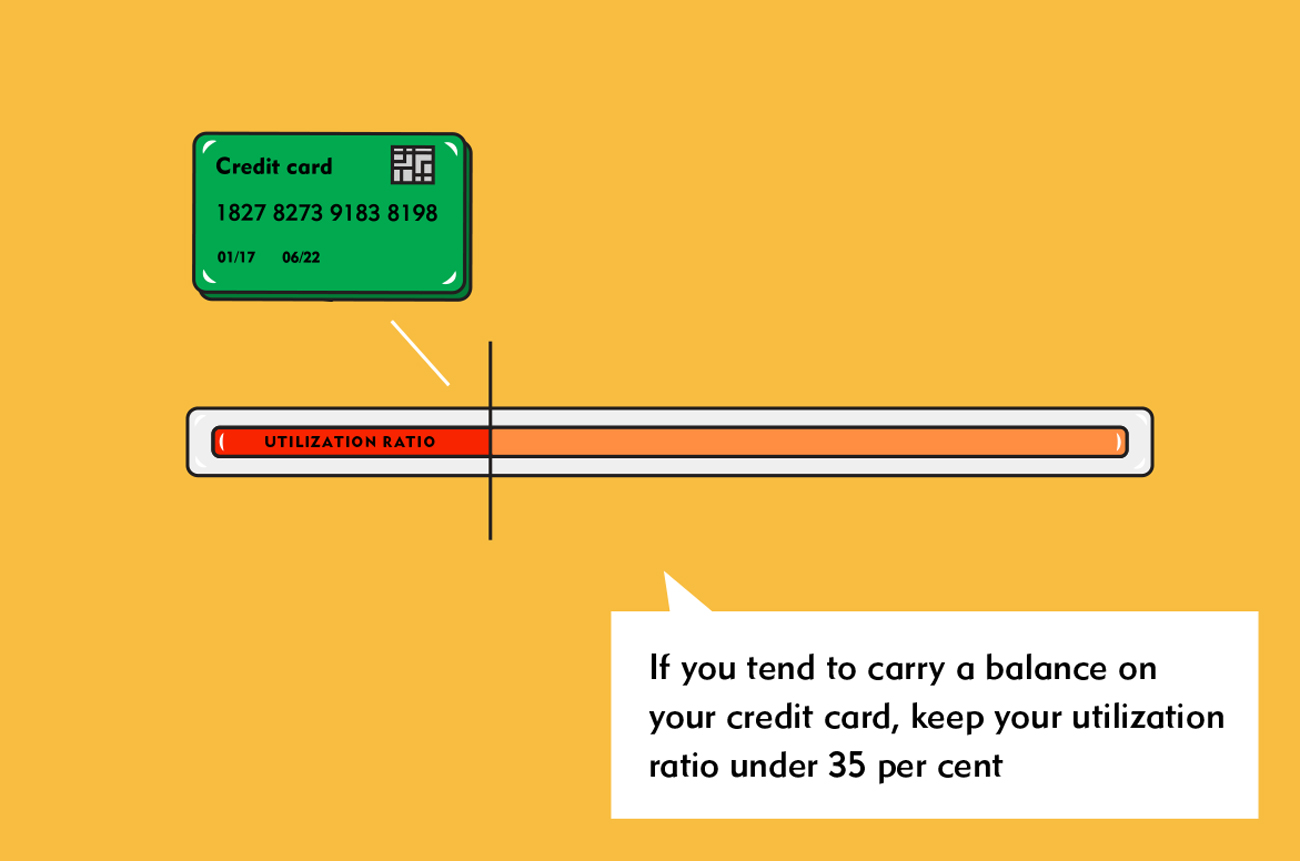

If you’re not so good at paying your credit card off every month...

If you tend to carry a balance on your credit card, try to keep it under 35 per cent.

1. This is close to the magic number for your utilization ratio and will help you get a strong credit score.

Most of this really comes down to your own self-control and ability to self manage your spending to keep yourself in check. If you struggle with that you might want to consider working on a budget, and separating your fixed costs and your “spending money”. A really easy way to do that is with a ‘Spending Account’ like the MogoCard* (now in beta). It’s coming to the public real soon, and it’s gunna be liiiiiiiife changing. Well, we think so anyway.

The most important step in all of this? Know your credit score. If you haven’t signed up for a MogoAccount yet, sign up now, and get your free credit score** with free monthly updates.

**Free credit score is provided by Equifax and is only available to MogoAccount holders that have passed identity verification. The Equifax credit score is based on Equifax’s proprietary model and may not be the same score used by third parties to assess your creditworthiness. The provision of this score to you is intended for your own educational use. Third parties will take into consideration other information in addition to a credit score when evaluating your creditworthiness.