How to improve your credit score and why it matters

One of the awesome things about signing up for a MogoAccount is that you get your credit score for free (paid for by us, provided by Equifax Canada). Oh btw, if you want to get your score somewhere else, be prepared to pony up. Yep, we're basically paying you to get a MogoAccount.

56% of Canadians have never checked their score. Not good. If you're one of them, create your MogoAccount to find out yours now. Knowing your credit score could help you get access to lower loan rates in the future, mortgages—and can be a big part of your dating life.

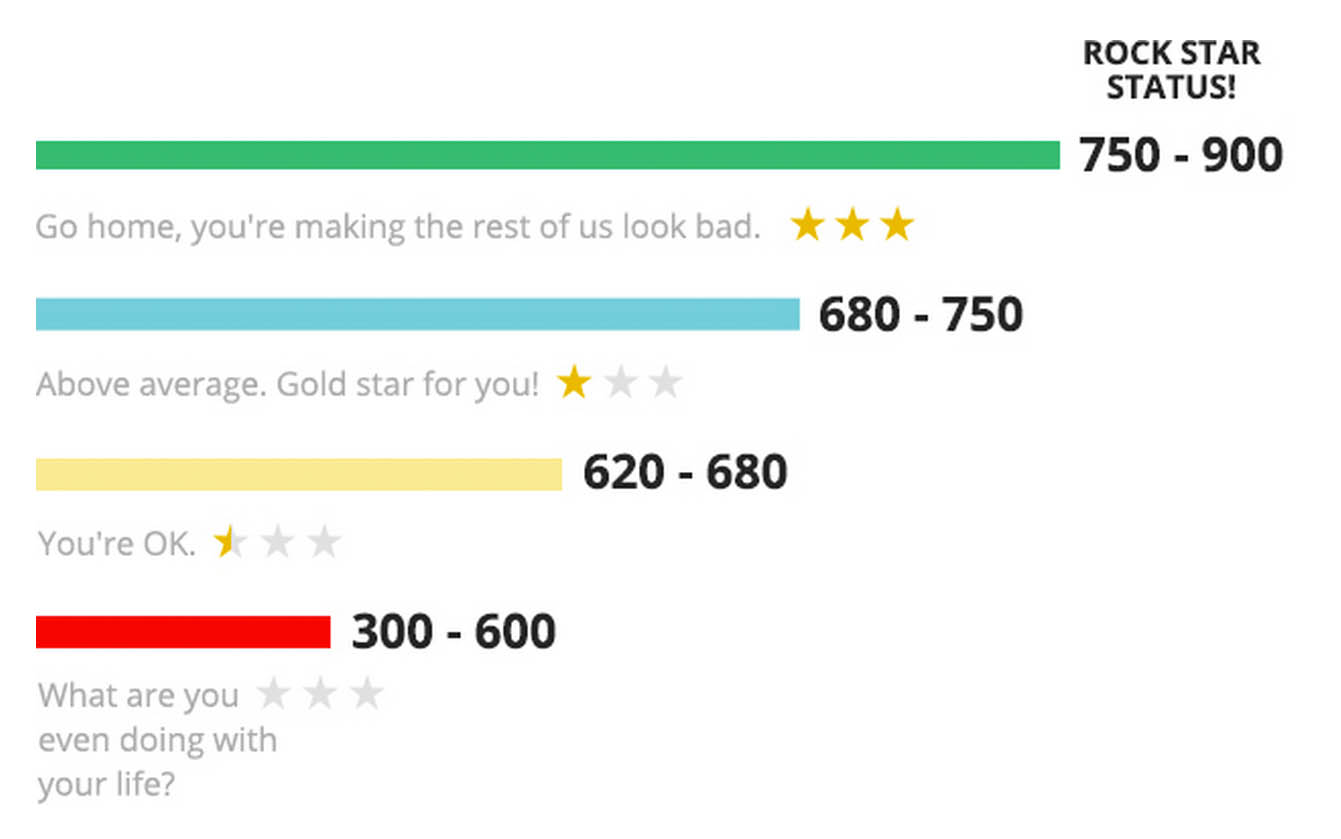

What’s your credit score and where does it fall on the scale of zero to hero?

Want to improve your credit score? Here’s what to look for:

Fraud or mistakes on your credit bureau. Make sure that everything on the report belongs to you and that the info is correct.

If you spot something, it’s time to contact Equifax Canada or Transunion—and do it right away as it can take a while to resolve the issue. An alternative (and quicker way) to get mistakes fixed is to have the creditor who made the mistake deal with Equifax Canada directly to update it.

Now that we’ve given you an out to blame your crappy score on a mistake, it’s time to look at other ways to fix your score.

Your credit report is basically your financial report card. You need to be enrolled in credit to get marks on this report card and you need good attendance and behaviour to get a high score. Most lenders want to see two forms of active credit for at least two years. The longer the history reporting, the better. But you don’t need to be weighed down with debt to show a credit history.

How?

Tip: don’t just pay your minimum payment on a credit card—otherwise you’ll be in debt forever.

Example: If your credit card limit is $1000, don’t go over a $700 balance.

When you dodge debt like it’s a drunk dude with halitosis, your account could get sent to a third party to recover the money you borrowed from the original lender.

The Fix: If you see any collections* reporting on the public records section of your credit report, contact the collection agency and pay them right away. But that’s not the most important part—ask the collector to have the history of it removed from your credit bureau right away!

*Collections can be things like phone bills, cable bills, parking tickets, and any other unpaid debts that aren't reporting with your other debts in the payment history section of your credit bureau.

Vancouverites: FYI, a city parking ticket will hit your credit bureau report as a collection if it isn’t paid in about 90 days.

In work, play, and credit, one truth remains: being promiscuous will earn you a bad reputation. Multiple hard credit checks in a short time could drop your score a little. Don’t fret too much though, credit inquires only account for about 10% of your score. I actually think it’s better to shop around and end up with a better rate (even if it means having your credit pulled) than only look at one option because you’re worried about your credit.

Chantel Chapman is Mogo’s Financial Fitness Coach. She teaches you how to be an adult, and is also the host of our Adulting 101 events. With over a decade’s experience as a mortgage broker, Chantel recognized a need for financial education with many of her first-time homebuyers, so she began creating custom content to help guide them. Chantel is the founder of Holler For Your Dollar, a consulting firm that jump-starts anyone who’s ready to dive into the world of Adulting or entrepreneurship. Her role at Mogo puts her skills to use creating and teaching digestible, yet educational financial literacy content geared to millennials and daring entrepreneurs.

Check your rate to get: