Student Loan Interest Suspension

What does this COVID-19 relief measure mean for your debt?

Do you have a student loan? Did you just survive a global pandemic? Do you want some good news?

Yes?

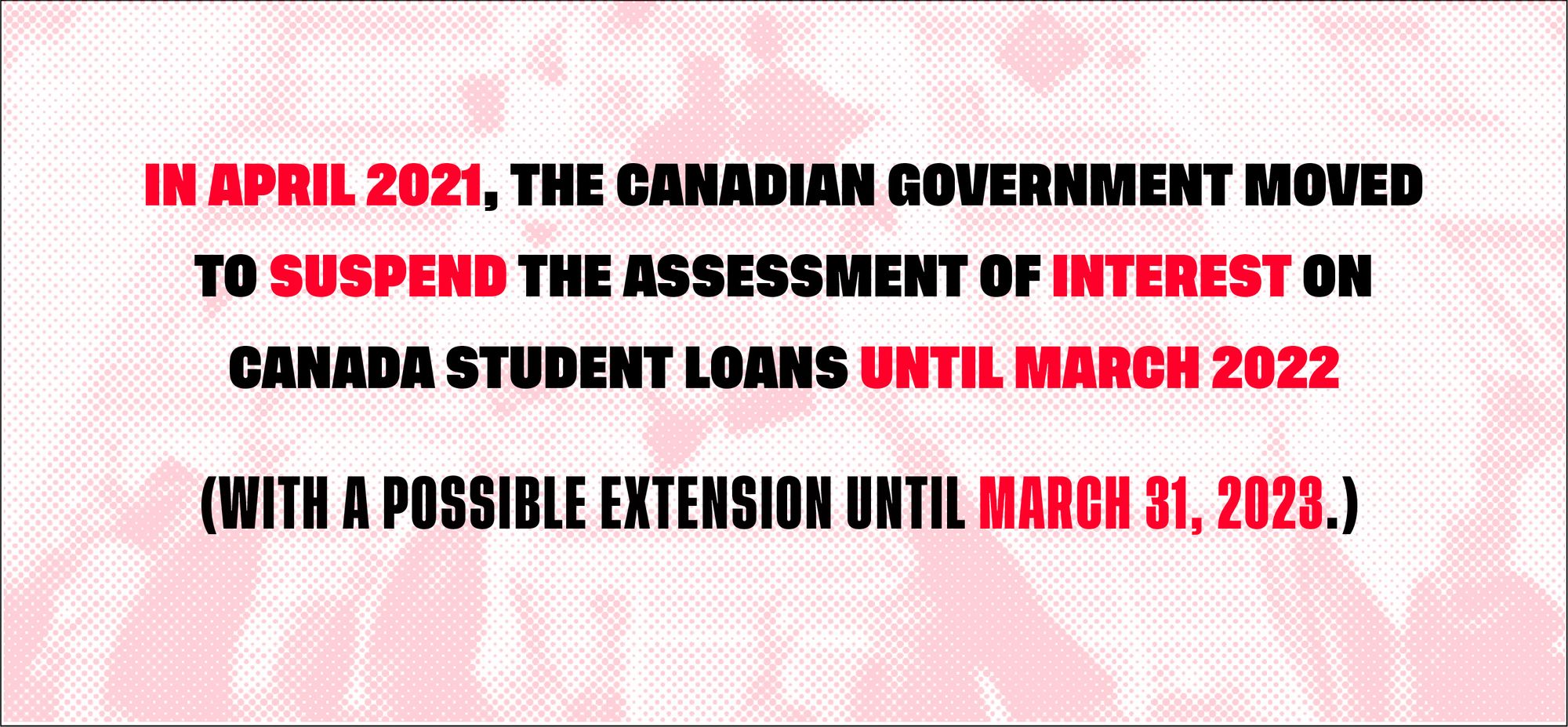

We got ya: in April 2021, the Canadian government moved to suspend the assessment of interest on Canada Student Loans.

Finally, some much needed breathing room. Find the details and how this change might impact you below.

Canada Suspends Student Loan Interest Until 2022

Here are the facts. As of summer 2021, student loan interest on Canada Student Loans is suspended until March 31, 2022. With parliamentary approval, this suspension will be extended further, until March 31, 2023. Woohoo!

This means that for this period, your Canada student loan will not accumulate any further interest. This is really good news.

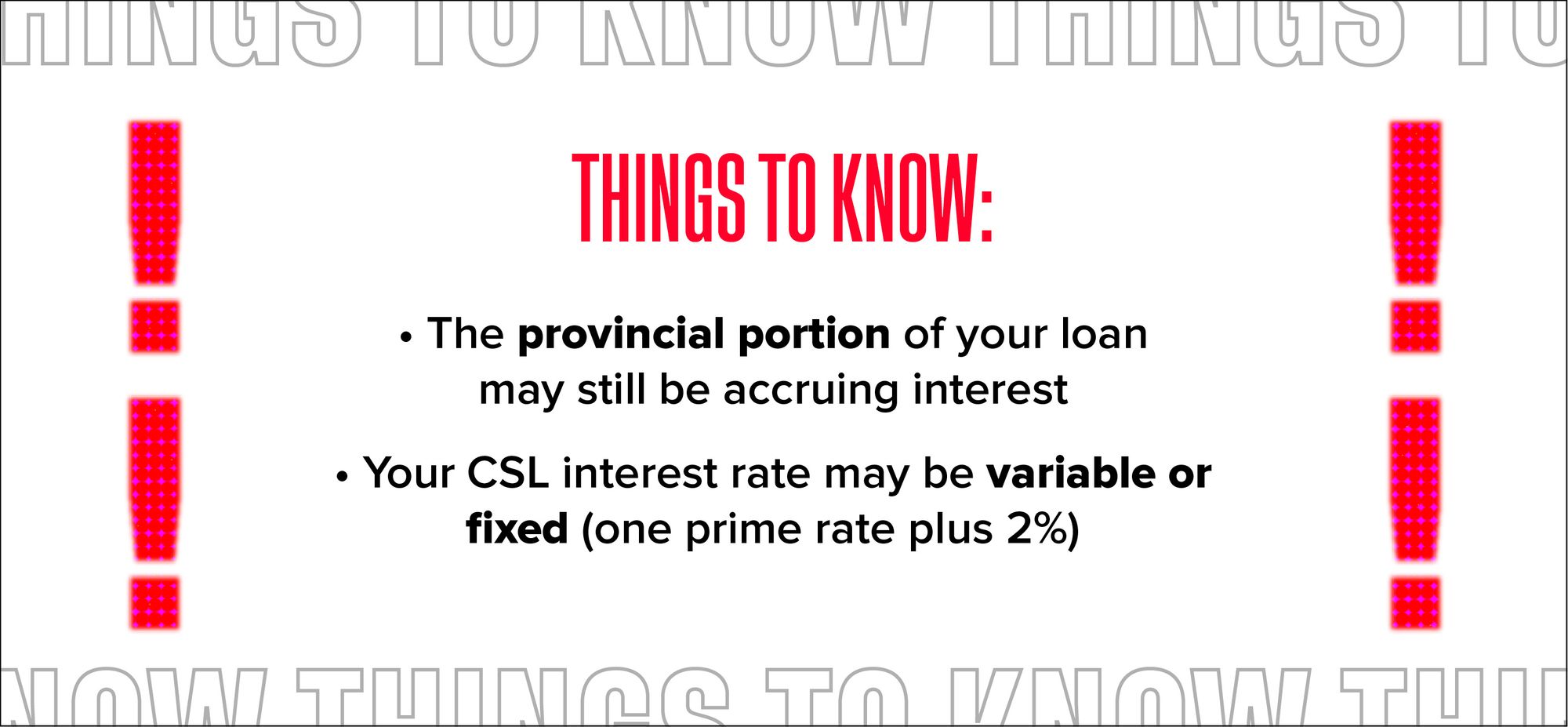

Don’t forget, though, that many student loans are a combination of provincial and federal loans, and the provincial interest rate may still apply. Log into your student loan portal to check your own loan’s composition.

What is an Interest Suspension?

When the government offers you a student loan, they expect you to pay it back plus interest. When setting up your loan, you’re able to choose which type of interest you’d prefer. There are two options:

- A variable, floating interest rate that tracks with the prime rate in Canada, or

- A fixed interest rate equal to f the prime rate plus 2%

The prime rate is calculated by the interest rates of the 5 largest Canadian banks. The highest and the lowest prime rates are removed, then an average of the remaining 3 is used. The current prime rate in Canada is 2.45% at time of writing.

An interest rate suspension sees no interest assessed on your remaining principal balance. This basically means that if you aren’t able to make any payments because of COVID-19, your debt won’t grow because of interest in this period.

What Does This Mean for My Debt?

If you haven’t yet, you should read this post on choosing whether to start saving for retirement or paying down your debts first.

What does the interest suspension mean for your debt? You can take two approaches that are diametrically opposed to one another, and are both good options.

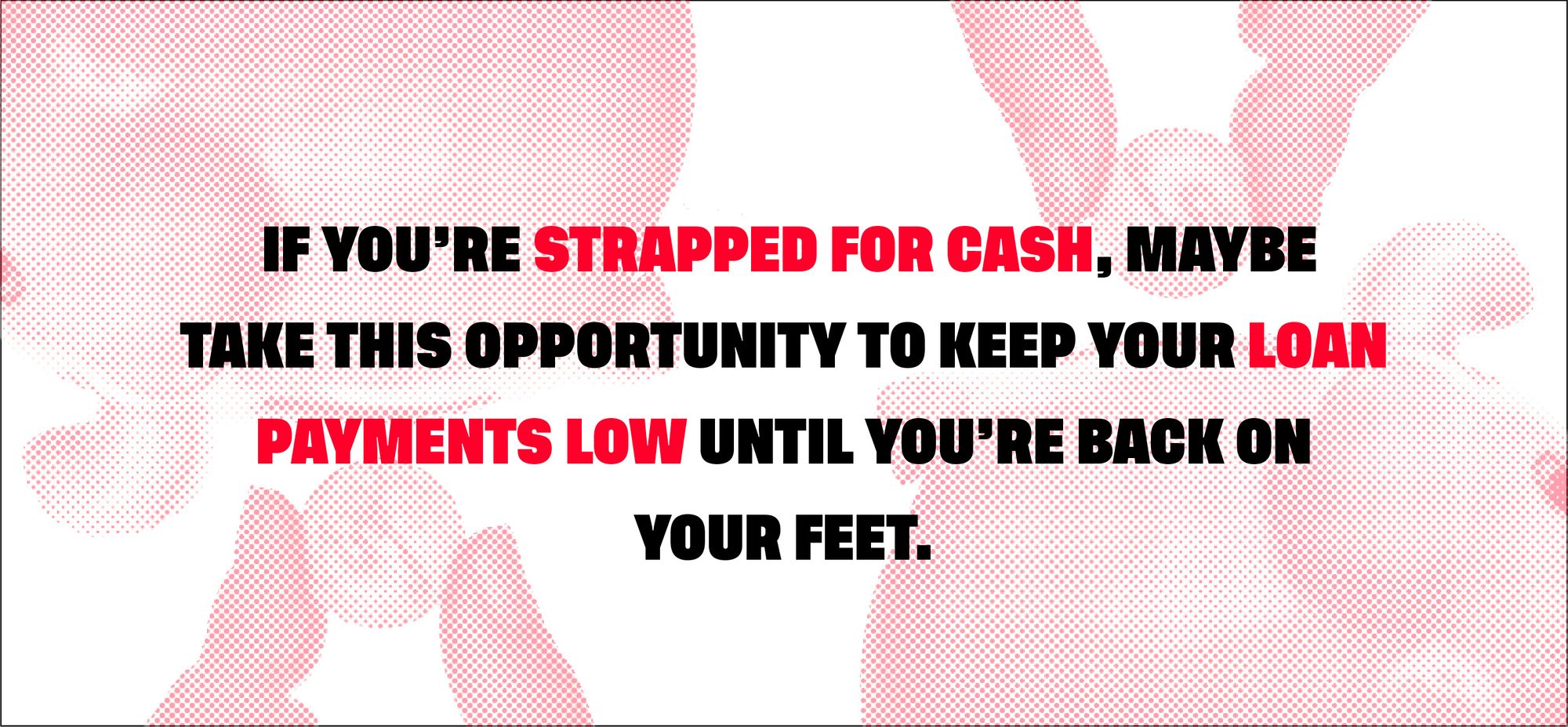

Take it Easy

With no interest assessed on your loan, if money is tight, you can use this period as a bit of relief. Talking to the government about what you can afford right now is always a good idea; if you’re out of work or struggling to make ends meet, there are relief measures available to you.

As such, if you’ve got more expenses than you know what to do with, just continue to make your agreed upon maintenance payments.

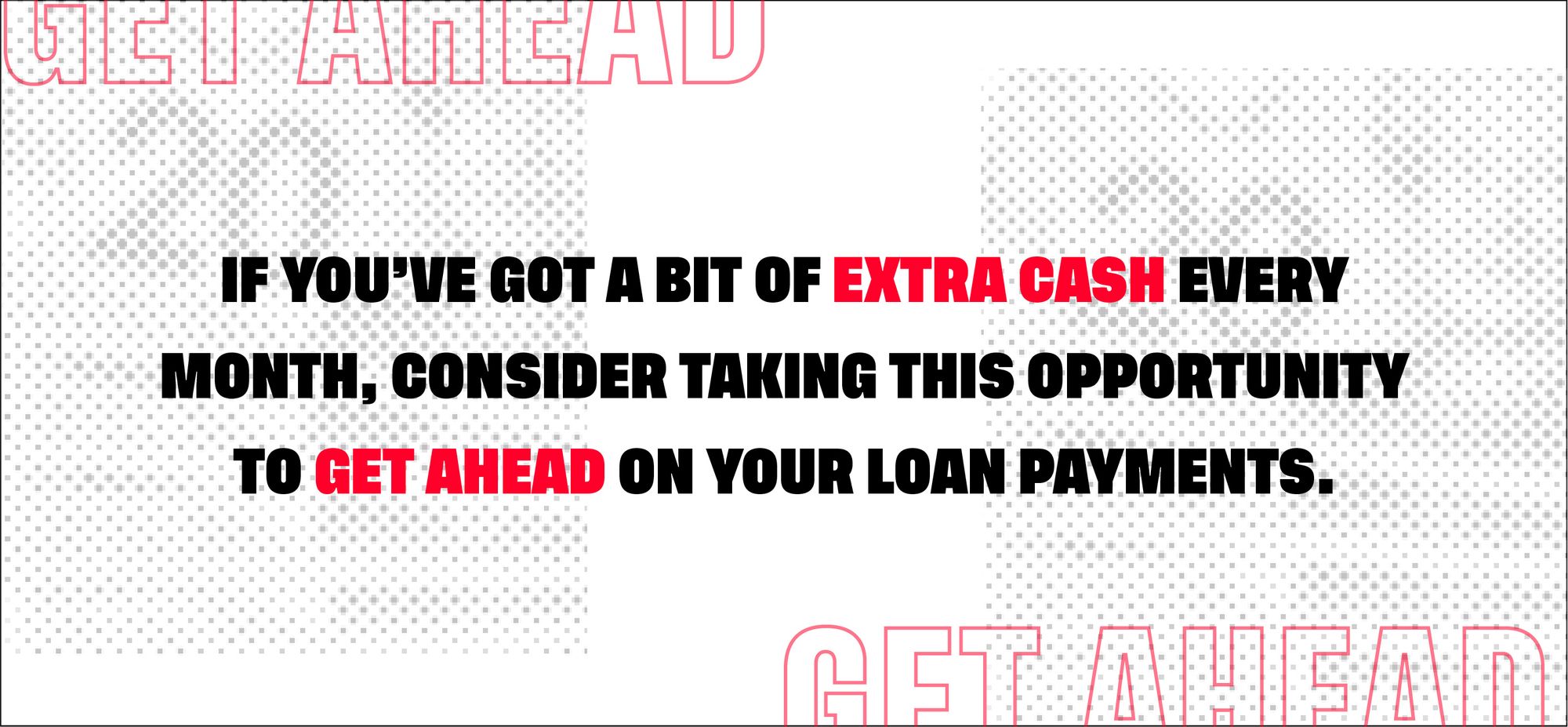

Get Ahead

Alternatively, if you have some spare cash each month, this period where interest is not being assessed represents an opportunity to get ahead. Paying your loan back more quickly while interest is suspended means more of your payments will go onto your principal balance.

Shrinking your principal balance means that when interest comes back, it will be assessed against a smaller amount. This could help you save on interest payments over the remaining term of your loan.

Either of these two options are good; how you decide to take advantage of the interest suspension is up to you.

Student loans are big, slow burns; with typically lower interest rates, it’s normal to pay them off over the course of 20 years. But with these relief measures in place, it’s important to consider how you might get ahead. You got this.

This blog is provided for informational purposes only, is not intended as financial advice, and is not meant to suggest that a particular financial strategy is suitable for you. If you’re unsure about a particular financial decision, you may wish to obtain advice from a qualified professional.