3 ways to improve your credit score

The higher your score the better. It’s used by lenders and financial institutions to determine whether your credit-worthy or not. In general, a low score could mean you’re declined on a loan or receive a higher interest rate, while a higher score allows for lower interest rates and better options when it comes to things like getting a mortgage and borrowing money. Your credit score number basically tells lenders how likely your are to repay money you borrow, based on how you’ve handled your financial obligations in the past.

• 47% of Canadians don’t know where to check their credit score

• 81% of Canadians don’t realize that an employer may check their credit score when being considered for a job

• 61% of Canadians don’t know that landlords often look at credit scores as part of a rental application

• 51% of Canadians don’t know that small business lenders look at credit scores when approving a small business loan

3 things that can help improve your score

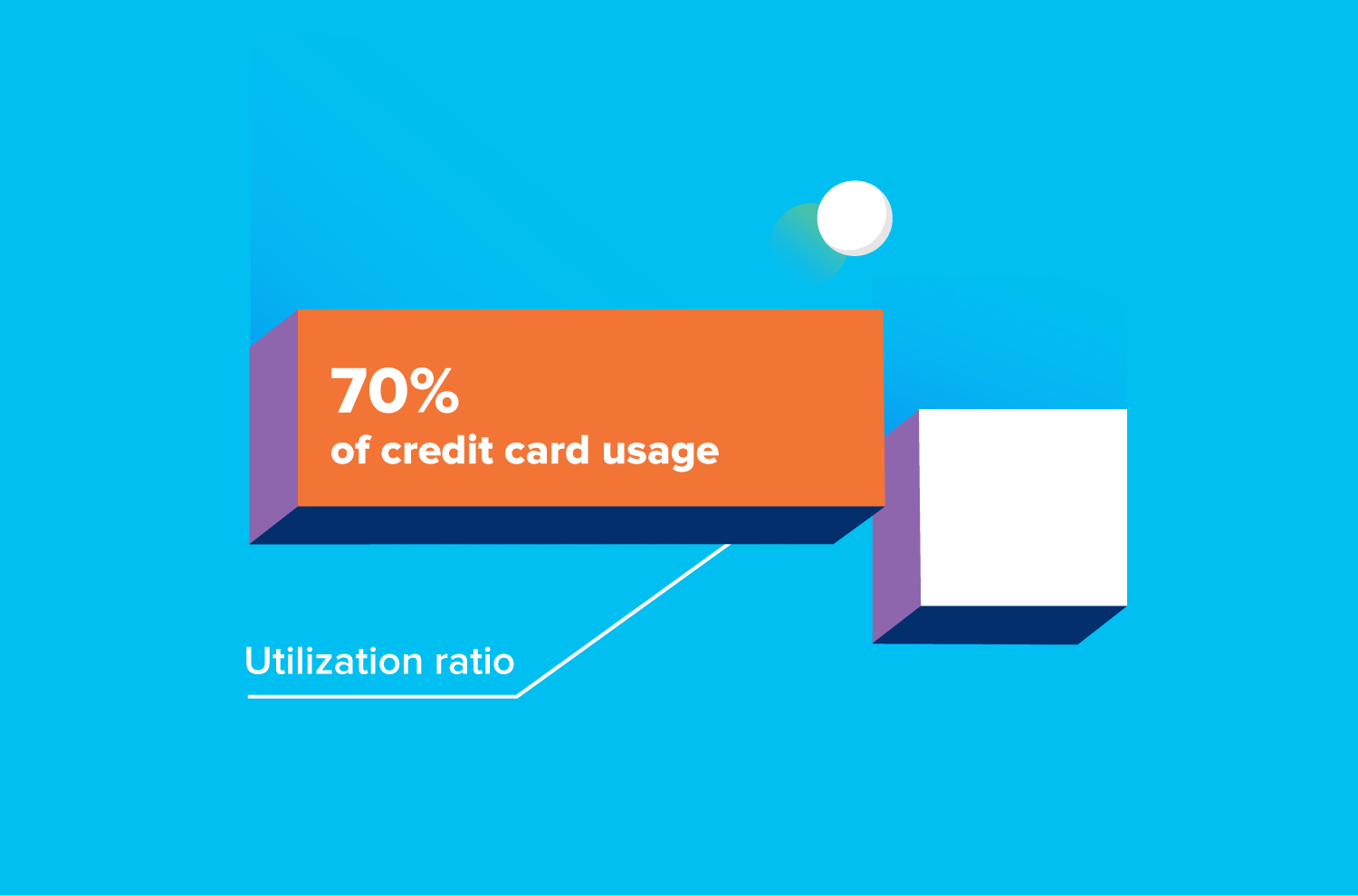

1. Practice good utilization ratio

A quick way to improve your credit score is to start practicing good utilization ratio habits. Once you start doing this, it could improve in as little as 30-60 days. If your credit card limit is $1,000 and your balance is $1,000, your utilization ratio is 100 per cent — and this not good in the eyes of the credit bureau. Credit bureaus base credit scores on behaviour with credit. If you're constantly maxing out your credit cards, it could imply that you're not far away from defaulting on your minimum payments. It looks like your income is stretched. Set an imaginary limit of 70 per cent and don't go over that. Doing this will keep your credit score healthy. For example, if your credit card limit is $10,000, don't borrow over $7,000.

2. Think twice about closing an unused credit card

It may seem like a good idea to close a credit card that you’re not using, or have paid off and are trying not to use. But, closing a card, or leaving it inactive can negatively affect your credit score. This goes back to the length of credit factor that the credit bureau reports on which makes up 15% of your credit score. Instead of closing the card, use our #NetflixandChill tip. Use the card for a monthly subscription, like Netflix or Spotify, and set up an automatic monthly payment from your bank account to ensure it’s covered. Then throw that card out of sight, and give it some chill out time. This trick will also improve your utilization ratio and payment history, since you’ll be staying far under your limit, and making on-time payments.

3.Consolidate credit card debt

Credit cards are considering revolving debt; meaning when you pay them down you can keep borrowing against them. This type of debt is psychologically proven to keep people in debt. Many revolving credit products allow you to pay back only the interest, which is a major reason why so many people find themselves stuck in what feels like an endless cycle of debt. If you’re like 46% of Canadians* and you carry a credit card balance every month, you could benefit from a personal instalment loan to help get out of the revolving debt cycle. Unlike credit card debt, an installment loan has a specific term and requires you to pay back interest and principal in every payment, which means you have a set deadline for paying it off and getting out of debt.