Are You Headed Toward Millionaire Status?

Keen to join a growing number of millennial millionaires? We’ve got tips for you.

Today, millionaire status is attainable for more Canadians than ever before. Once a far-off ideal reserved only for the rich and famous, financial independence for us normals is here to stay. The key? Consistency. It’s that simple.

From curbing your spending with a budget to saving and investing, getting on track to becoming a millionaire is becoming easier than ever. Learn more below.

Becoming a Millionaire

Wondering how to become a millionaire? You’re (obviously) not alone. Finding financial security—not having to worry about your finances every day—seems like the ultimate respite. Lucky for all of us, millionaire status is closer than ever.

At Mogo, we believe financial independence is contingent upon Canadians having the information and knowledge they need to make informed decisions for themselves. This guide isn’t definitive, and everyone is different—so you must do your own research and choose wisely.

But these tips aren’t wishy-washy—they’re actionable. Why? Because the best way to become a millionaire is to start saving today.

The first step: create a budget and determine how much you can save every month. We like the 50/30/20 budget, but everyone is different. Once you’ve determined your ability to save, consider applying these tips to create a strategy. And just like that, you’re on your way. 🚀

How can I save money?

If you’re like many millennials, you’ve probably still got the same bank accounts your parents set up for you when you started earning an allowance. While the standard chequing account/savings account split worked for ten year olds, they’re probably not going to get you to millionaire status alone.

When choosing how and where to save your money, it is crucial to find the option that is going to make your money work the hardest for you over time.

Two of the most popular savings products in Canada are Tax Free Savings Accounts (TFSAs) and Registered Retirement Savings Plans (RRSPs). TFSAs allow you to earn tax free income. RRSPs are tax-deferred accounts, and shelter your income until you withdraw it, ideally in your retirement, when you’re in a much lower tax bracket and thus pay less tax on your savings.

Both have annual contribution limits, but both can hold investments, and as such, can grow much faster than simple contributions and compound interest alone. This is what we mean by making your money work hard: maximizing wealth growth while maintaining a comfortable contribution level.

Investments are serious business and you must do your own research to decide what is right for you. Here are some helpful tips on choosing between a robo-advisor or an actively managed fund, and here’s an explainer on how to invest.

Where should I invest?

There are many different investment products available to Canadians. Here is a rundown of a handful of popular options. If any sound interesting to you, we encourage you to investigate further with the help of a professional advisor.

Exchange Traded Funds (ETFs)

ETFs are a great way to build wealth over time. By buying into ETFs, you become the owner of many fractions of many stocks. Because these are generally low cost and generally well diversified, ETFs can have some of the best returns over time with some of the lowest risk to investors.

ETFs may be tracked to certain indexes, or contain a more random collection of stocks, bonds, and other financial instruments.

In working toward millionaire status, one effective strategy includes incorporating consistent investment in ETFs over the course of decades. With steady returns, this cash can seriously add up.

The bottom line: ETFs are typically lower risk, but usually grow more slowly.

Cryptocurrency

Investing in cryptocurrency like bitcoin is part of many wealth building strategies, but it should be regarded with caution. Cryptocurrency is incredibly volatile, and while it may skyrocket up to $100,000 per unit on a Monday, it could be worth $0 by Friday.

A safer option to invest in bitcoin? Consider dollar cost averaging, or, investing lower amounts of money over a longer period of time. This way, if the market tanks, you may be less likely to lose a huge amount.

Then, if crypto crashes, you’re not out any of your own cash.

The bottom line: cryptocurrency may bring huge returns, cryptocurrency may also bring huge losses. Not a safe get rich quick scheme.

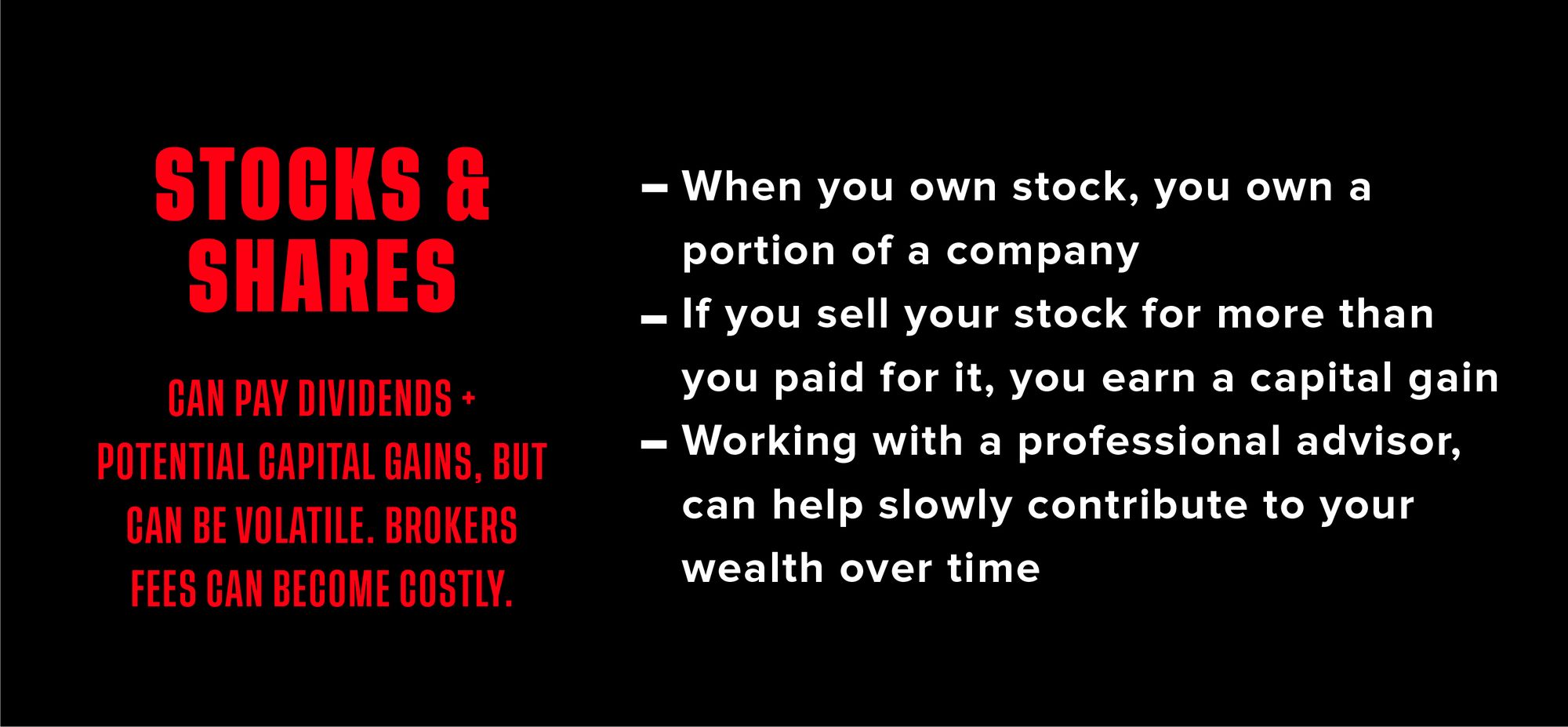

Stocks and Shares

Stocks are the subject of many-a-meme. #stonks

But investing in stocks, usually through a broker (though they will charge a fee!), can super power your wealth building. When you own stock, you own a portion of a company, and are paid dividends. If you sell your stock for more than you bought it for, you earn a capital gain.

Similar to cryptocurrency, investing in stocks can be more volatile; but working with a professional advisor, or a robo-advisor, to set an appropriate risk level can help slowly contribute to your wealth over time.

The bottom line: investing in stocks can pay dividends and potential capital gains, but can be volatile. Brokers fees can also become costly.

Bonds

Investing in bonds means you’re lending a company or government your money in exchange for a guarantee that, at the end of a set period, you’ll be repaid in full plus some interest.

Bonds have different risk levels, depending on the business or government you’re buying them from. If the bond is riskier, you can expect higher interest rates—but sometimes the risk is not worth the reward.

Common types of bonds include corporate bonds, federal government bonds, provincial government bonds, and municipal government bonds.

The bottom line: bonds aren’t free of risk, but you can opt for slower growing, low-risk options. The right bond option will depend on your comfort with risk.

How long will it take to become a millionaire?

Here’s the rub: these tips won’t make you a millionaire overnight.

These strategies make use of the “miracle” of compound interest, where performance compounds—and thus accelerates—over time. So you’ll probably see less growth in your savings in the early years than you will in your later years.

This is just the way it is. The average Canadian can’t afford to save a ton every month. One of the best ways to become a millionaire is to plan on reaching your target just before or at your retirement age.

Should I pay down my debt first?

If you hold debt, you may want to consider paying it down aggressively before you begin saving. Why? Because the cost of the interest on your balance owed may effectively cancel out your savings growth in the early years.

If you hold a personal loan, credit card debt, payday loan, auto loan, or another type of shorter-term, higher interest loan, you might want to think about paying it off sooner, perhaps redirecting your savings budget towards erasing your debt.

If you hold a student loan or a mortgage that will take many years to pay off, it’s more likely you should maintain steady payments while getting to work on your savings, too.

Here’s a blog post that explores this balance.

A Guide to Hitting a Million

That millionaire life is within reach for so many Canadians. The key is getting started today. Seriously—the earlier the better.

To recap:

- Make your budget to determine how much you can afford to save every month;

- Make your money work hard for you by investing responsibly;

- Ensure you keep your debt under control, and then

- Enjoy being a fancy shmancy millionaire.

Mogo offers a few tools that can help you on your journey. This is a product plug, yes, but we really think they can help!

You could also consider our new BFF, Moka, a super sleek app that offers a fully-managed investment portfolio.

You can do this! Get started today and don’t forget about us when you’re a millionaire, eh?

This blog is provided for informational purposes only, isn’t intended as investment advice, and isn’t meant to suggest a particular investment or strategy is suitable for any particular investor. Every situation is unique and if you’re unsure about an investment or financial strategy, you may wish to obtain advice from a qualified professional. Nothing herein should be considered an offer, solicitation of an offer, or advice to buy or sell securities. Buying and selling bitcoin is risky and you may suffer losses. The price of bitcoin is highly volatile and speculative. You should never invest more in bitcoin than you can afford to lose. Past performance is no guarantee of future results. Always do your research and never invest more than you can afford to lose. *Trademark of Visa International Service Association and used under licence by Peoples Trust Company. Mogo Visa Platinum Prepaid Card is issued by Peoples Trust Company pursuant to licence by Visa Int. and is subject to Terms and Conditions, visit mogo.ca for full details. Your MogoCard balance is not insured by the Canada Deposit Insurance Corporation (CDIC). MogoCard means the Mogo Visa Platinum Prepaid Card.