3 ways to improve credit score

Your credit score affects you more than you think — especially when it's time to get approved on exciting life milestones, like buying a car or home. Lenders look at your score to determine your creditworthiness, or how good you are at handling your financial obligations. It’s how they determine how big a mortgage or loan (or how high a credit card limit) to offer you and at what interest rate. Having a low score could result in getting approved at higher interest rates — or even being declined. Many landlords look at your score when considering renting to you, and some employers are even requesting info on your credit score before making you a job offer.

A few different factors make up your score, with payment history, utilization ratio, and length of credit topping the list, followed by types of credit and inquiries.

Whether your score is stellar or needs some TLC, there are some easy ways to improve it and ultimately rule it.

Here are 3 ways to get you started:

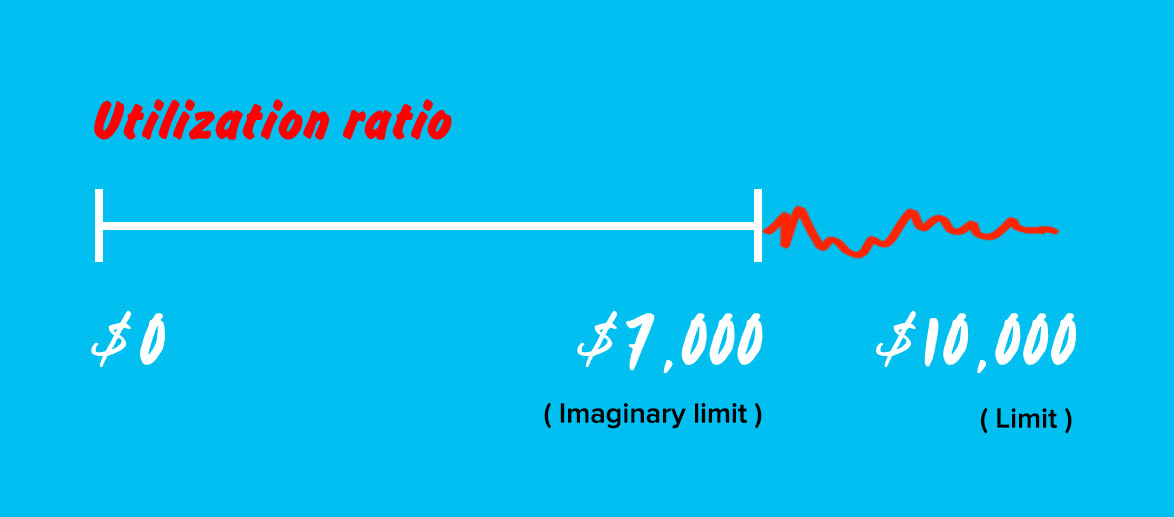

Nail your utilization ratio

Your utilization ratio is how much of your available credit you’re using, or your level of indebtedness. For example, if your credit card limit is $1,000 and your balance is $1,000, your utilization ratio is 100 per cent — and this not good in the eyes of the credit bureau. If you're constantly maxing out your credit cards, it could imply that your income is stretched. And, your utilization ratio makes up about 30% of your overall credit score rating, so it can impact it pretty substantially.

![]()

RULE YOUR SCORE TIP:

Don’t ever let your utilization ratio go over

70 per cent.

Set an imaginary limit of 70 per cent and don't go over that. Doing this will keep your credit score healthy. For example, if your credit card limit is $10,000, don't borrow over $7,000.

Fixing your utilization ratio is one of the fastest ways of improving your score, so if you have a habit of accumulating credit card debt, make a payment and your score can increase quickly. Then, make sure you practice the 70 percent rule and you’ll be rocking your utilization ratio in no time.

Ditch your late payments

Approximately 35% of your credit score is made up of your payment history, so missing even one payment can hugely impact it. Your history of missing payments stays on your credit bureau for 6 years. But don’t worry, once you start making your minimum payments regularly, as time goes on it impacts your score less and less as you prove you can be a responsible adult.

![]()

RULE YOUR SCORE TIP:

Don’t miss minimum payments. Ever.

It doesn’t matter if it’s a $4 minimum payment or $400, when you miss a payment (whether it’s your credit card, line of credit, or loan payment), it’ll have a negative impact on your credit score.

Consolidate your debt

If you’re stuck in the cycle of credit card debt (ie/ regularly max out your card, and don’t always make your payments on time) you’re really hurting your credit score.

You’re not alone. In 2016, Canadian households owed a total of $2,028.7 billion, an increase of nearly $30 billion in the last three months of 2016. $596.5 billion of that is in consumer debt, largely made up of credit card debt. And, 46% of Canadians carry a credit card balance every month.

Credit card debt is what’s considered revolving debt, meaning you can immediately re-borrow what you pay back on principal. This type of debt has been psychologically proven to keep people in debt, because it makes it easy to spend—it’s less psychologically painful to swipe a card than physically use cash—and encourages overspending. According to a recent study, consumers spend 12-18% more when using a credit card as their payment method.

One way to break the vicious revolving debt cycle is by consolidating it with an installment loan.

Unlike revolving credit, your personal loan would have a term and require you to pay back interest AND principal in every payment, which means you have a set deadline for paying it off and getting out of debt.

![]()

RULE YOUR SCORE TIP:

Consolidate revolving debt with a loan.

Start ruling your finances by downloading the MogoApp

The free Mogo app lets you see your credit score right away and your score is updated every month for free. Aside from the free credit score you’ll also get access to many other benefits and financial products.

![]()