The difference between a Mogo pre-approval and approval

But before we answer this question, here’s a quick rundown of what it’s like to apply for a loan at Mogo.

How it works at Mogo

Once you’ve signed up for a MogoAccount, you’ll automatically get a pre-approval decision from us that gives you a loan amount and rate. If you like this offer, you can take this offer by filling out a few more details quickly and confirming you want the loan. At that point, we’ll take a closer look at the information you’ve provided and give you an official loan offer. Oh and if you don’t need a loan, no sweat—you don’t need to take it.

Okay cool. Now let’s get into how a pre-approval is different from an approval.

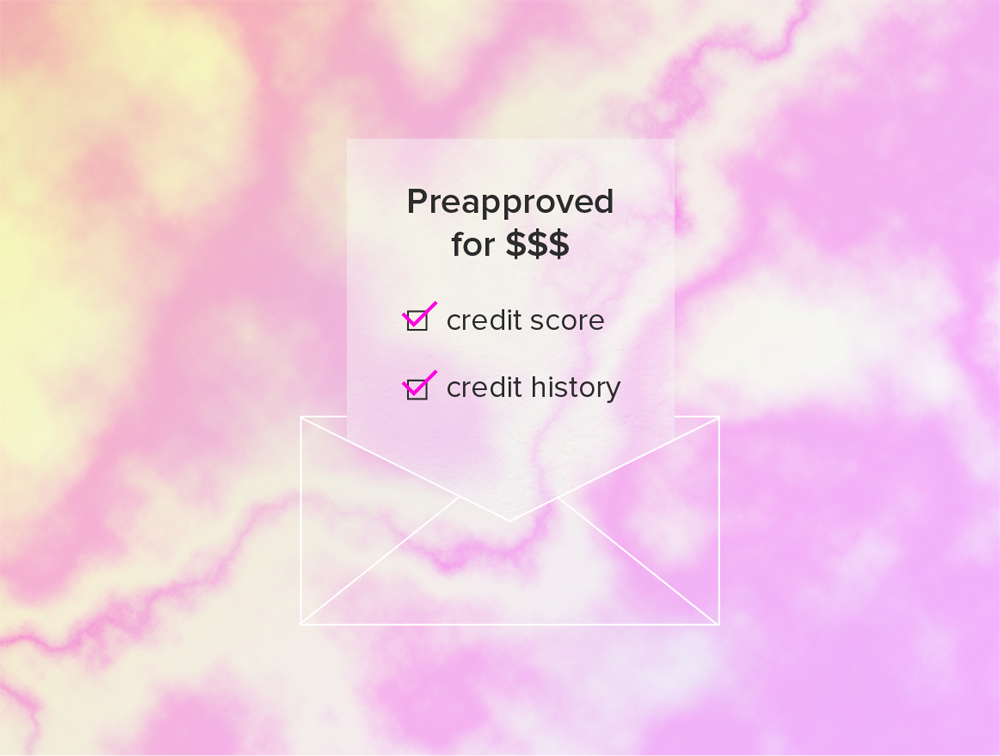

The loan pre-approval process

When you’re looking to get a loan, you usually get pre-approved first. Even if you’re not looking for a loan, you might get offers online or in the mail saying that you’ve been pre-approved for a certain amount of $$$. To give you a pre-approval offer, the lender might look at your credit score and credit history to make sure that on a high level, everything checks out. Having a pre-approval means that you’ve passed most of the requirements needed to get that loan—not that the loan is guaranteed!

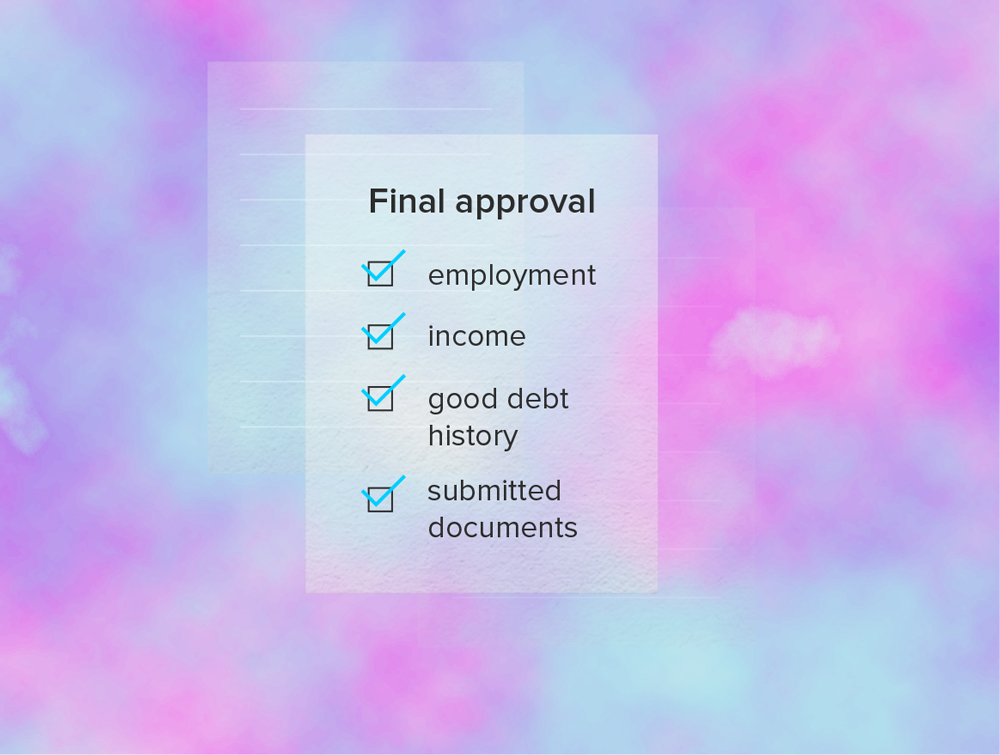

The final loan approval

So the lender has made you a pre-approval offer. Cool. But before giving you a final approval, lenders do a much more thorough check. At this point, they’ll also be verifying the personal information you’ve submitted (like your employment info). This is to make sure that you are who you say are and not some fraudster wanting to borrow money under your name. And also to check that you’ve been telling the truth about your ability to pay that loan back... because that’s kind of important when you’re lending money.

So, given all of this, here are some common reasons why you might get denied after you’ve already been pre-approved:

![]()

![]()

![]()

![]()

That’s why Mogo’s pre-approval offers come with boring legal stuff:

Pre-approval is based on information submitted in your MogoAccount application and/or other information that indicates you could meet our underwriting requirements. Your pre-approval for credit remains subject to our credit approval process which includes but is not limited to income and identity verification and validation of information submitted through the Mogo.ca website. To meet our underwriting requirements further documentation may be requested from you. Minimum income requirements may apply for some products. Approval is not guaranteed and we reserve the right to deny services to you.